Low interest rates have made borrowing money cheaper than ever, but interest rates could start to rise in the next 12 months. If you’re paying off a mortgage, it could affect your outgoings and the full cost of borrowing.

We’ve experienced over a decade of very low interest rates. That’s been good news if you’re borrowing but has negatively affected savers. However, this could change as the economy begins to recover from the effects of the pandemic.

The Bank of England (BoE) first cut interest rates to record lows following the 2008 financial crisis as a way to support the economy during the recession that followed. In November 2017, the rate was increased from 0.25% to 0.5% and increased again to 0.75% in August 2018, suggesting the central bank would gradually raise rates to “normal” levels. However, this was reversed as the extent of the Covid-19 pandemic became known in 2020.

In March 2020, the BoE made two interest rate cuts and the rate has stood at an all-time low of 0.1% ever since. This cut has played a role in keeping the economy afloat during the uncertainty caused by the pandemic.

Record growth forecasts could lead to an interest rate rise

At the last BoE meeting in June 2021, the Monetary Policy Committee voted to keep interest rates at 0.1%.

However, the BoE also forecasts that the UK will experience its fastest period of growth in over 70 years in 2021. According to a report from the BBC, the economy is forecast to expand by 7.25% this year, although this follows the biggest contraction in 300 years in 2020.

The economy bouncing back is likely to mean the BoE will not introduce negative interest rates, which were being discussed. It also suggests that interest rates will start to rise in late 2021 or 2022. Any rises announced are expected to be gradual, so it’s unlikely we’ll return to “normal” interest rates any time soon. Yet even a small change in interest rates can have a significant impact on borrowers.

The impact of an interest rate rise on your mortgage

A mortgage is often the largest form of borrowing anyone takes out. As the amount borrowed is large and is usually paid back over decades, a change in interest can mean buying your own home becomes far more expensive.

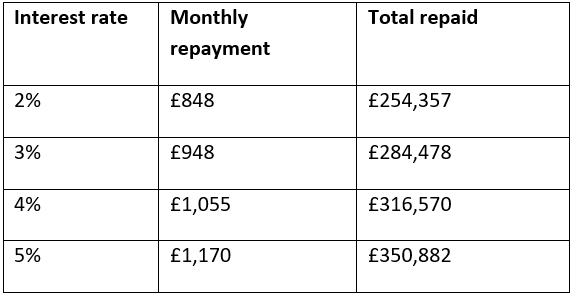

Let’s say you borrow £200,000 to buy your home and have a mortgage term of 25 years, the table below highlights how a change in interest affects your monthly outgoings and the overall cost of borrowing.

Source: Money Saving Expert

When you first think about it, the difference between 2% and 5% may seem relatively small, but the compounding effect on interest means it adds up. Over the full term of your mortgage, you’d pay almost £100,000 more in interest if your mortgage rate was 5% rather than 2%. With interest rates expected to increase, it’s important you understand the impact it could have on your finances and the cost of borrowing.

If interest rates begin to rise, whether you’re affected will depend on the type of mortgage you have:

- Tracker mortgage: This type of mortgage tracks the BoE’s base rate. So, if the central bank increased the interest rate, your mortgage’s interest rate would rise by the same amount.

- Variable mortgage: A variable mortgage works in a similar way to a tracker mortgage. However, it follows the rate set by your lender rather than the BoE. If the base rate increased, it’s likely your lender would also increase their rate.

- Fixed mortgage: With a fixed mortgage, your interest rate is fixed for a defined period. If interest rates changed, this wouldn’t affect your mortgage until your existing deal comes to an end.

So, is it time to fix your mortgage interest rate?

If you choose a fixed-rate mortgage, your outgoings won’t be immediately affected by rate rises. With interest rates low, fixing the rate now could make sense and save you money. However, if rates didn’t rise or even fell, you’d end up missing out. With no guarantees, it can be difficult to know what to do.

Don’t rush into choosing a mortgage. It can have a huge impact on your finances and it’s worth taking some time to consider. It’s not just the interest rate that’s important either. Depending on your circumstances things like being able to overpay or port your mortgage to a new property can be valuable.

If your current mortgage deal is coming to an end, please contact us to talk about your needs and to find the right mortgage for you.

Please note: This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.